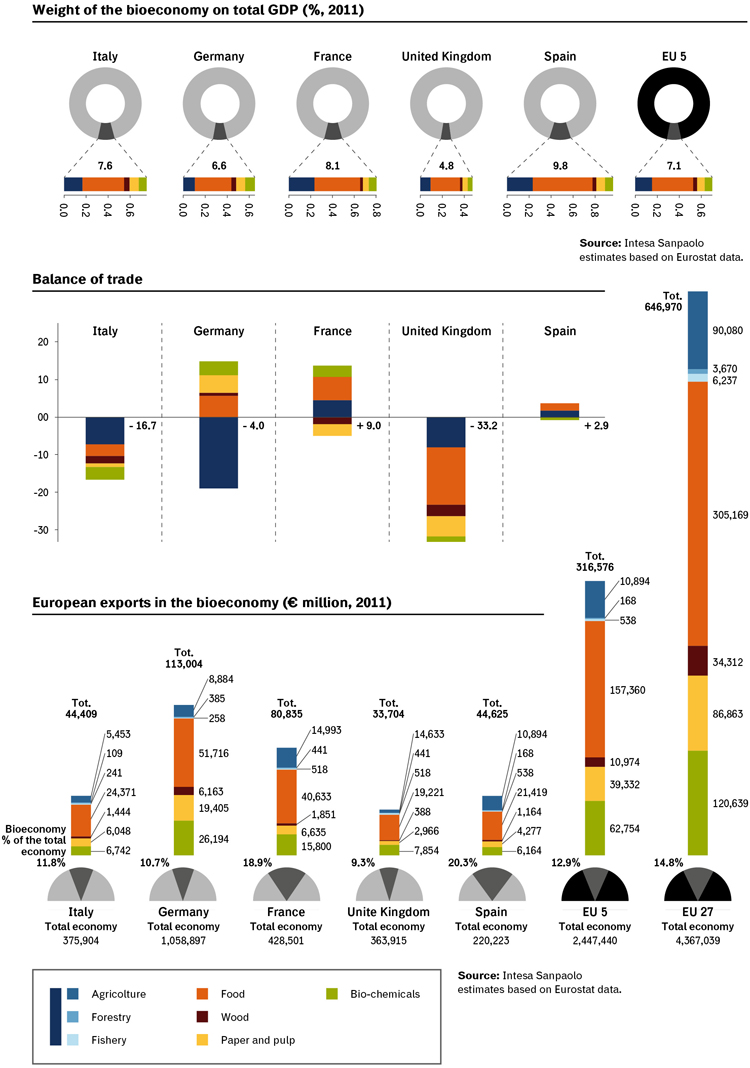

We now know that in Italy the bioeconomy is worth €241 billion and employs approximately 1.6 million people. Such figures are provided by Intesa Sanpaolo Think Tank based on a thorough analysis carried out in Italy, Spain, France, Germany and the UK (the so-called EU 5 countries). It also provides the value of world exports (US$ 2.1 trillion in 2012) for the first time.

In this special list of the European bioeconomy, Italy is in third position. Germany is first with a production worth €330 billion and France second with €295 billion. Spain is fourth (€186 billion) followed by the UK (€155 billion). In these five countries, the bioeconomy is worth €1.2 trillion and employs 7.5 million people (the total of people working in this sector in the EU-27 countries amounts to 18 million).

But how has Intesa Sanpaolo Think Tank come up with these figures? According to Stefania Trenti and Serena Fumagalli, the two authors of the report, “The calculation of the value of the bioeconomy was carried out using available statistical data both on the value of production and employment and exports. As for agriculture, silviculture, fishing, wood, paper and food industries, official statistical information already provides the bulk of the data. Calculating the value of the chemical industry was rather more complex”.

Such complexity derives from the need to understand which chemicals are already obtained from renewable sources. To this end, “The analysis was carried out with the help of a biotechnology expert working at the nova-Institut in Germany who was asked to identify chemical products that could be manufactured from renewable materials utilizing existing technologies. This list, based on the highest level of disaggregation available, enabled us to identify not what is currently produced with renewable materials but rather the economically sustainable potential production with currently available technology”.

This has proved that biotechnology is already an important sector both in Italy and in Europe. It obviously takes into account the whole agricultural and food industry as well as silviculture, even if not all agricultural products or wood are used as biomass for the industrial sector. But this is what was taken into account by the EU when in 2012 it launched its biotechnology strategy, providing the first data for this meta-industry in the EU-27 countries: it has a total turnover of €2 trillion and employs 22 million people.

“Our analysis,” the two authors continue “outlines the importance of the bioeconomy in Spain where it represents 9.8% of GDP employing 1.3 million people. This is mainly due to the agricultural and food sectors, but Spain’s production of biochemicals is also higher than the EU-5 average. The bioeconomy plays a relevant role also in France where it represents 8.1% of GDP, again mainly due to the agricultural and food industry while the role of other sectors (paper, wood and biochemicals) is weaker than average. So France and Spain are the only two countries with a balance of trade for bioeconomy products.”

It appears that it is always the agricultural and food industry that leads the way. What about Italy? How is the country that should supposedly base an important share of its economy on its food excellence doing? Here, the agricultural and food industry has a negative balance of trade. The UK is in the same position while Germany, at least as far as the food industry is concerned, has a positive balance of trade.

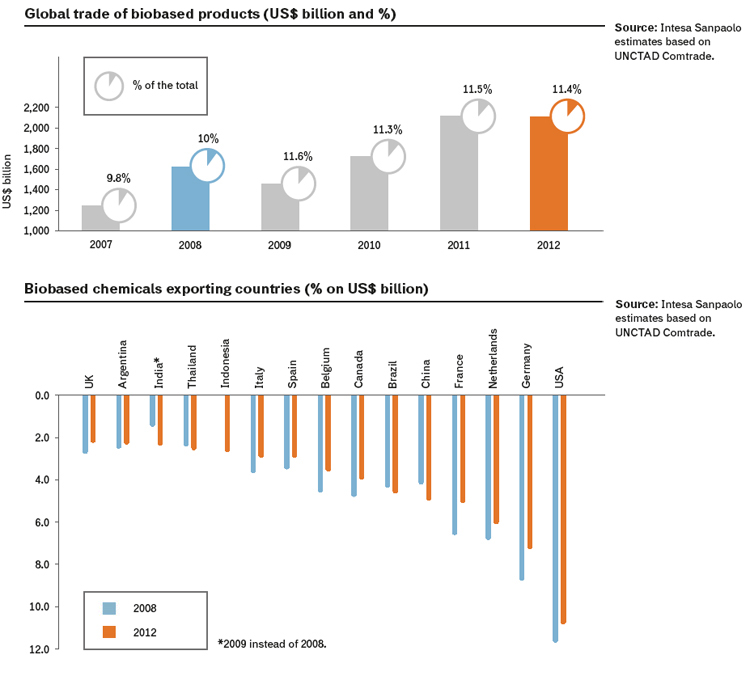

In 2012, global exports of bioeconomy products (according to Intesa Sanpaolo Think Tank list) – “The last year with sufficient global trade statistical data” the authors highlighted – amounted to $2.1 trillion, that is 11.4% of global trade, a rapidly expanding share compared to 8.9% in 2007. Food products, worth 1.85 trillion, represent 45% of total exports. As a whole, the agricultural and food industry makes up two thirds of the total, followed by biochemicals amounting to 16% of exports. These data put into perspective the growing importance of the industry’s use of renewable sources.

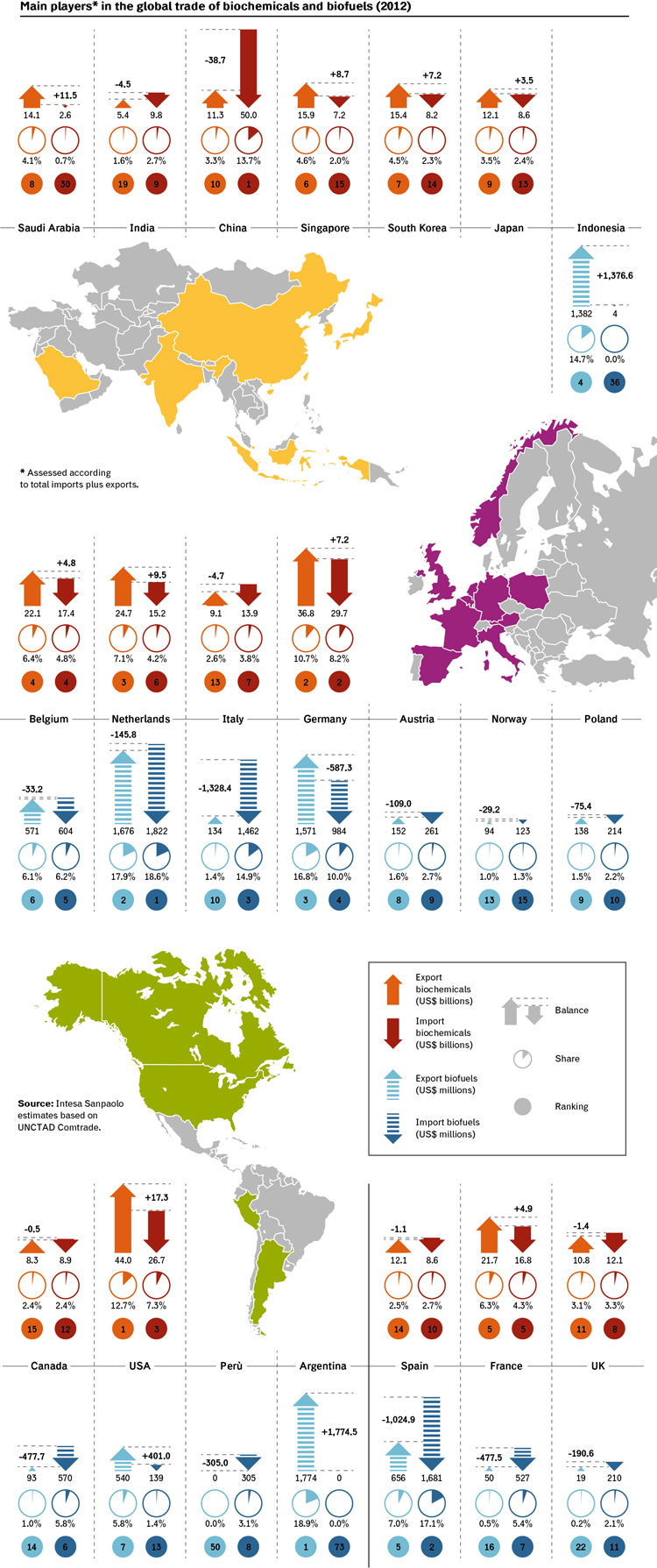

The main players include the USA, Germany, the Netherlands, France and also China and Brazil, with shares higher than 4% of total global exports.

“As seen in many other sectors”, Ms Trenti and Ms Fumagalli claim “even in the bioeconomy the role of mature countries seems declining in favour of emerging countries such as China, Brazil, India, Indonesia and Thailand that are winning larger shares of the global export market.”

From an import point of view the picture is different: in 2012, the main global importing country was China – with a share nearing 10% of total imports, rising steeply compared to 2008 data – followed by the G7 countries, the Netherlands and Belgium.

As for the biochemicals global market, the two main players are the USA and Germany with high shares of global exports. Even despite their high imports, this enables them to enjoy a positive balance of trade. China ranks third, but it presents a negative balance of trade because it is the main global importing country of these products with a share of 13.7% in 2012.

Belgium, the Netherlands and France rank very high amongst the exporting countries while Italy is only thirteenth with a market share of 2.6% and a negative balance of trade equalling $4.7 billion in 2012.

European statistical data also enabled Intesa Sanpaolo Think tank to estimate the value of the biofuel production in the EU 28 zone in 2013. A total of 8.5 million tons worth nearly €7 billion. In the same year, exports amounted to €351 million while imports came close to €1 billion, a negative trade balance just short of €600 million (865,000 tons). According to the two Italian researchers, “This sector is relatively closed to trade outside the EU 28, nearly all of its total production is destined to Europe and its characterized by a low import penetration”.