What Does the Concept of Bio-Based Economy Promise?

The idea of creating a Bio-based Economy is exciting for the material sector: It promises to introduce new chemicals, building-blocks and polymers with new functionalities; to develop new process technologies such as industrial biotechnology; to deliver solutions for Green and Sustainable Chemistry and Circular Economy. It is supposed to help mitigate climate change through the substitution of petrochemicals by materials with lower GHG emissions. It could bring new business opportunities, investment and employment to rural areas, foster regional development and support SMEs. And finally, the whole utilization of biomass could be optimized by new biorefinery concepts. The European Commission has stated that: “Biorefineries should adopt a cascading approach to the use of their inputs, favouring highest value add and resource efficient products, such as bio-based products and industrial materials, over bioenergy” and that “the advantages of the products over conventional products range from more sustainable production processes, to improved functionalities (e.g. enzyme-based detergents that work more efficiently at lower temperatures, save energy and replace phosphorus) and characteristics (e.g. biodegradability, lower toxicity)” (European Commission 2012).

One of the latest document, the Communiqué of the first Global Bioeconomy Summit 2015 in Berlin, states that: “Bioeconomy is the knowledge-based production and utilization of biological resources, innovative biological processes and principles to sustainably provide goods and services across all economic sectors. [...] Innovation efforts will need to focus on increasing and maintaining the biobased value. [...] In many countries, small and medium-sized enterprises are key drivers of biobased innovation. [...] Bioeconomy policy should therefore empower small and medium-sized businesses to participate in bioeconomy development.” (GBS 2015)

What Have we Reached so Far?

Not a lot. The amount of biomass used in the chemical and plastic industry in the EU has been almost stagnating over the last ten years. Only the bioenergy and biofuel sectors has developed well thanks a strong regulatory framework and high incentives from national regulations based on the Renewable Energy Directive (RED) and the Emission Trading System (ETS). This non-level playing field is well known and the impacts on the development in the chemical and plastic industry are strong: higher prices and difficult access to biomass.

Today’s most important market pull instrument in the bio-based sector is the RED, which creates artificial demand for bioenergy and biofuels. In terms of investment and market volume, this has been very successful. However, several problems of the current framework have started to become apparent over the last few years (Carus et al. 2015):

- Many Member States are not on track with meeting their renewable energy quotas;

- Sustainability certification of feedstocks is only part of the answer as the pressure on ecosystems and the resulting problems of (indirect) land use change and biodiversity loss persist;

- The system of multiple counting for certain feedstocks remains an issue, as well as their classifications as waste, residue or co-product;

- Feedstock bottlenecks have appeared for the bio-based material sector due to the increased and unbalanced demand for biomass;

- The existing RED framework does not take resource efficiency, cascading use and circular economy into account and can even contradict those concepts through incentives for the energetic use of biomass and especially through classification of certain biomass types as being waste, when they can in fact be used for other material purposes.

In a nutshell, the high-value bio-based economy is not picking up any speed. This is caused, among other things, by the framework conditions created by the RED, which systematically prevent new developments and investments in higher value added applications, such as bio-based chemicals and materials, by only supporting energy use of biomass (Carus et al. 2015).

This view is confirmed by recent research in the FP7 project BIO-TIC (2015): “This means, for example, incentives for bioenergy (...) may hinder the most efficient use of biomass in higher-value material use. Cascading systems should be promoted by a level-playing field. The market, left to its own devices, will ensure the maximum value use of biomass alone. Where subsidies distort the market to the extent that this becomes a problem for other industries, the problem should be tackled at the regional or national level.”

From an environmental viewpoint, the successful bioenergy and biofuel expansion has to be more regulated to avoid negative impacts such as direct and indirect land use changes (LUC and iLUC), food insecurity and the deforestation of US forests for pellets to cover the demand of the European bioenergy sector: “Every year, European countries import millions of tons of wood pellets to burn as fuel. [...] The demand for wood pellets in Europe has increased dramatically since the introduction of the European Union’s 2009 Renewable Energy Directive. However, forestry is strictly regulated in Europe, so European countries have turned to the southeastern U.S. to supply their rapidly-growing demand for biofuel. [...] The demand just keeps growing. Some estimates predict that in five years’ time from now, Europe will be importing as much as 70 million tonnes of wood to burn. Is it possible to keep up with this astronomical demand without damaging U.S. forests in the process? [...] Not all wood-based biofuel comes from sustainable sources like sawdust and tree trimmings. There’s simply not enough of this remnant wood to go around. Many wood pellet mills in the southeastern U.S. source from mature bottomland hardwood forests. Mississippi, Alabama, Georgia, North Carolina and Virginia are among the states most impacted. Often, multiple pellet mills will harvest from the same patch of forest, creating a hot spot of logging pressure in that area. Bottomland hardwood forests are a unique type of wetland ecosystem that grows around rivers and streams. [...] The degradation and removal of forests, especially highly productive wetlands like these, can also have huge and sometimes unpredictable impacts on the carbon cycle. Europe’s efforts to reduce carbon emissions may simply be disrupting the carbon cycle in new ways” (Yoon 2015).

Status

Bioenergy and biofuels have developed very well in the RED framework, but in many Member States the incentives are decreasing and new investment activities are low or get delayed. Depending on the achieved share, in some Member States the volume of bioenergy and biofuels is still growing, in others it is constant or even decreasing.

In the chemical industry, the overall bio-based share has remained at about 10-12% for many years, showing no relevant increase at all.

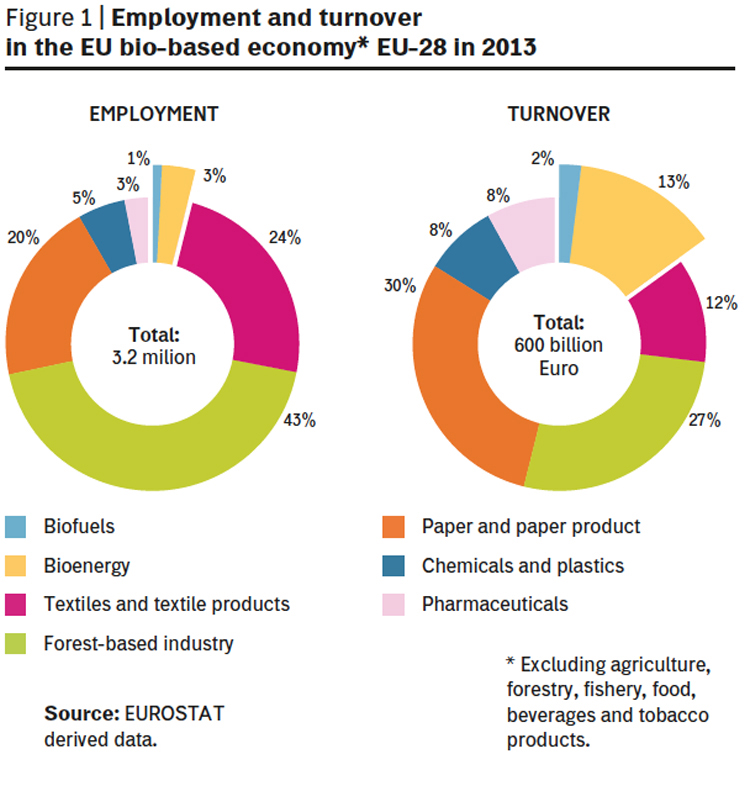

Figures 1 shows employment and turnover in the different sectors of the bio-based economy. At the first look, it is surprising that despite of the described development there is more employment in the bio-based chemical industry than in bioenergy and biofuels together, and wood-based material applications show much more employment and turnover than bioenergy from woody biomass. The reason is shown in figure 2.

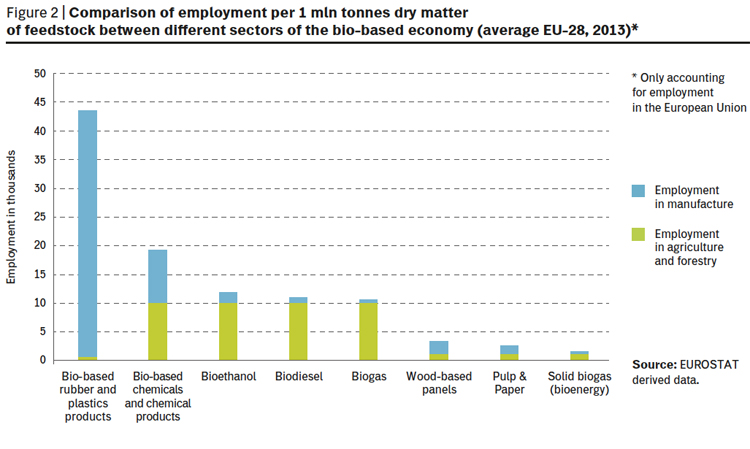

Figure 2 shows the employment per mln tonnes dry matter (tdm) of feedstock for different sectors of the bio-based economy. The green share shows the employment in agriculture and forestry. As expected, much more employment is linked to 1 mln tdm agricultural biomass than to 1 mln tdm wood. For the further processing to the final application, the blue share in the column, all material applications of biomass are responsible for much more employment than bioenergy or biofuels are.

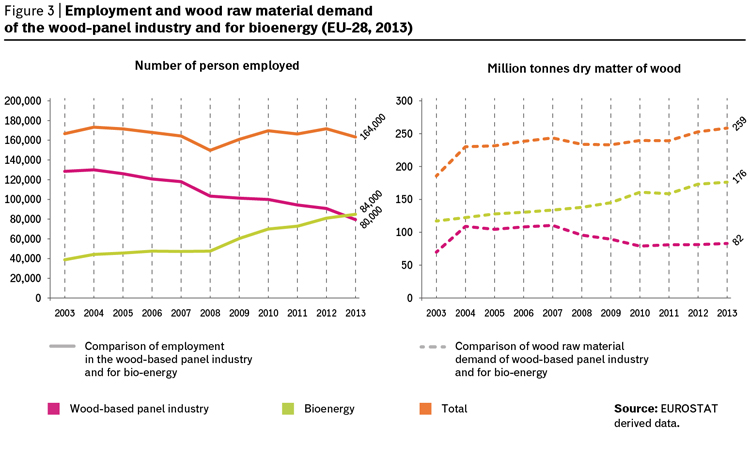

Figures 3 shows the development of the wood-based panel industry and the bioenergy from 2003 to 2013. Employment in bioenergy is growing year by year, mainly due to the incentive framework. By contrast, in the wood-based panel industry the employment is decreasing year by year. The competition to the bioenergy sector on sawmill by-products is not the only reason for this, but it is one of the main ones. Bioenergy incentives have driven up wood prices, and the non-incentivized European wood-based panel industry faces problems to pay the higher prices in competition to the world market of panels.

Figure 3 (left) shows the total employment in both sectors, and interestingly it is on exactly the same level in 2003 and 2013. And even more interestingly (see figure 3 right), to achieve this level of employment with a much higher share of bioenergy (70% in 2013 instead of 25% in 2003), the industry needs 80 mln tdm more wood as raw material, which accounts for an increase of 45%!

Outlook

Meanwhile, more and more political experts have come to the conclusion that it was a mistake to implement such a strong non-level playing field for the bio-based economy. It is expected that the next renewable energy regime for the period after 2020 will include less incentives for this sector and it is still open whether binding targets for Member States will be in place after 2020 at all.

What’s next? Often it is said that biofuels, especially bioethanol, are forerunners for chemical applications, preparing volume and infrastructure for the bio-based economy. Sounds good – but we should be careful not to immediately make the next mistake.

Bioethanol is mainly used as a forerunner for drop-in chemicals. For the overwhelming majority of new bio-based building blocks ethanol is no forerunner at all. Policy will again have a high impact on the development of the bio-based economy and should guide in a future-orientated direction.

Are Drop-In Commodity Chemicals the Next Step Forward or Another Dead end of the Bio-Based Economy?

At first look, drop-in commodity chemicals do not look too bad (Mathijs et al. 2015):

- They can directly substitute fossil-based chemical building blocks 1:1, so they can easily utilize the existing value and production chains as well as the infrastructure of the petrochemical industry;

- Meaning that implementation can be fast, with relatively low investment;

- Mature markets with potentially high substitution volume such as ethylene (from ethanol), propylene (from ethanol and biogas) and derived PE, PP, PET and PVC already exist;

- In many cases they have lower GHG emissions compared to their petrochemical counterparts.

But at a second look, drop-in commodity chemicals do not look so good (Mathijs et al. 2015, Iffland et al. 2015):

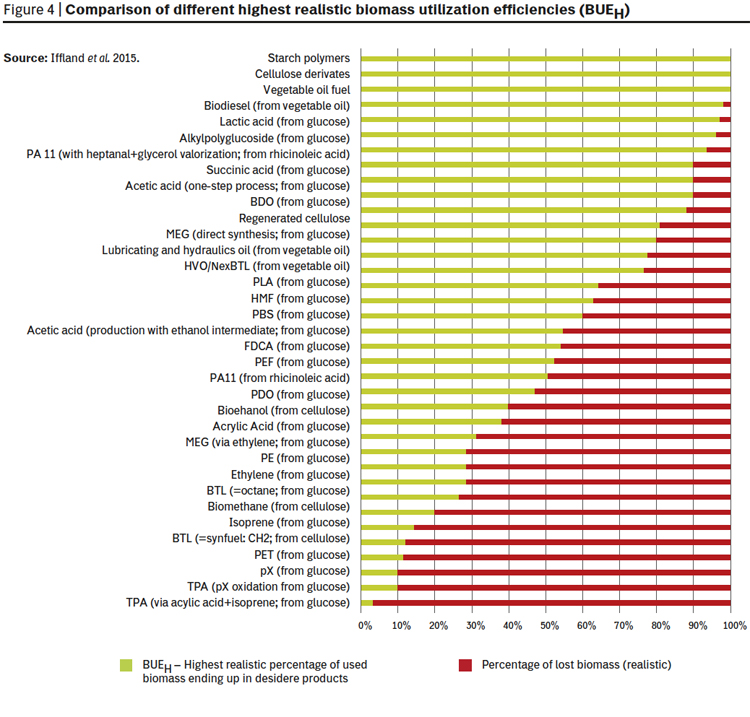

- The Biomass Utilization Efficiency (BUE) from feedstock to final product (meaning how much of the used biomass actually ends up in the product) is low, ranging between 25 and 50% only (Iffland et al. 2015);

- Respective technology of isolation and purification is required. In many cases, cost-effective fractionation and conversion technologies are still in their infancy;

- Drop-ins do not provide any new or additional functionalities compared to petrochemicals;

- They have to compete directly with petrochemicals that are produced at a low price;

- They give low value added to the biomass;

- To reduce the production costs, large-scale production is required (local feedstock supply hardly possible, impacts on availability, price for biomass and other sectors);

- But also large-scale production will suffer from higher costs for feedstock and processing compared to petrochemicals and will not be competitive (until the crude oil price will be very high);

- Implementation needs a strong commitment from policy and long-term incentives, and a strong commitment from society to receive long-term GreenPremium prices.

Would it not be better to make high-value chemicals with new functionalities for emerging markets and with a more efficient biomass utilization conversion? “Limited biomass should be used more efficiently: Do more value-added and create more employment – with less biomass” (Carus et al. 2011).

Bio-based drop-in commodity chemicals are biofuels’ brothers and sisters. This is both good and bad at the same time and we should be very aware of this. And we should take a thorough look at alternatives, which may be closer to the original promises of the bio-based economy (see below).

Two recent publications support this view on drop-in bio-based chemicals: “Every aspect of the wood must be mined for value, and the value extraction processes need to be designed for maximum synergy. In a fully integrated biorefinery, each stage builds on the previous and feeds the next. Such leading-edge biorefineries are however unlikely to emerge as long as they are driven by the idea of providing drop-in products that merely replace (one-for-one) those traditionally supplied by the petrochemical industry. [...] By narrowly focusing on the drop-in fit, producers have been unable to construct the kind of integrated process that utilizes all the side streams and by-products – thus having to carry higher total costs. [...] Insisting on drop-in adequacy, means too high a cost in preparing and processing the bio-materials, with considerable losses of biomass. A far better way is to drive biorefinery development towards recognizing the diverse character of the biomass and derive value in a holistic and integrated model. We believe this is the way for biorefineries and bio-products to be competitive without requiring subsidies” (NISCluster 2015).

Also the German Chemical Association does not believe in drop-in commodities from biomass: “The potential for growing additional biomass in Europe is very low compared to the rest of the world. Therefore, the high transport costs of biomass with low energy density speaks rather against importing large quantities of renewable raw materials to Europe for the production of commodities” (VCI 2015).

James Philp made an interesting and surprising proposal for bio-based drop-in chemicals in 2015. He is highly aware of the mentioned weak points of the drop-in commodities. But he also sees potentially high volumes linked to corresponding GHG emission reduction: “For the policy maker, replacing the oil barrel requires bio-based alternatives to the major petrochemicals such as ethylene and other short-chain olefins. However, trying to make a high-volume bio-based equivalent of a petrochemical suffers two large impediments:

1. Over decades the petrochemical equivalent has had its production process and supply chains perfected and the production plants have been amortised, so that it benefits enormously from economies of scale;

2. Bioprocesses are notoriously inefficient when it comes to scaling up to a level that can influence a market. [...]

Lower support for lower production volume, greater support for higher volume. This makes sense in the current policy setting as:

- Greater production volume means a greater contribution to national GHG emissions reduction targets;

- It should act as the sought-after R&D stimulus for companies to make process improvements that make further GHG savings.

[...] It specifically addresses high-volume, low value chemicals because these have the greatest impact in replacing the oil barrel and in emissions reduction. These are precisely the chemicals that are unattractive to the young bio-based industry as it is extremely difficult to synthesise them efficiently at scale in competition with the petrochemicals industry” (Philp 2015).

Coming from the priority of reducing GHG emissions, this proposal is consequent and logical. Although it sounds paradox to give long-time incentives for inefficient large-scale industrial processes with high volume instead of innovative, efficient and special applications, also suitable for SMEs. Also the potential volume of the new, non-drop-in solutions and drop-in fine chemicals should not be underestimated.

Can the absolute volume of GHG reduction be the only criterion when deciding on the future policy framework of the bio-based economy? And would it not then be the real question whether we should promote bio-based chemicals at all since in various studies it was clarified that there are significantly more cost-effective ways of GHG savings available such as thermal insulation in homes.

Taking any other parameters seriously such as relative GHG saving per tonnes of biomass, high biomass utilization efficiency (which means less biomass and cultivation area for the same amount of final product), innovation, investment and competiveness, employment, it makes no sense to develop possible incentives exclusively for drop-in commodities – drop-in fine chemicals and new chemicals should be included too.

Are Huge Lignocellulosic Biorefineries the Next Step Forward or Another Dead End of the Bio-Based Economy?

One of the great hopes of the European bio-based economy are huge lignocellulosic biorefineries. And here again, the big question is whether they are a solution or another dead end. These refinery concepts have several weak points and these points are also the reason why the implementation is so slow.

- Recent lignocellulosic biorefineries will produce high-priced C5 and C6 sugars for fermentation processes; the price is much higher than for sugar from sugar beet or sugar cane.

- The cost disadvantage would need to be balanced by the utilization of lignin, which is so far hardly feasible.

- Because of this situation, some experts propose to go to a really high scale: Utilization of one or even two million tonnes of biomass per year are necessary to overcome the cost issue through the economy of scale.

- This means that high investments are needed and no local feedstock supply is possible. Locations for such a high-scale biorefinery would be mainly limited to big harbours such as Rotterdam, Antwerp or Hamburg. And it still means high risks for selling the products at competitive prices, especially the lignin.

- Most concepts for these biorefineries focus on drop-in commodity chemicals such as bioethanol, mainly because of the production volume, existing infrastructure and incentives. For this, the structurally very complex cellulose polymer needs to be broken down to be processed into low-value commodities. Pros and cons of drop-ins were discussed in the last chapter.

- To implement those biorefineries, long-term incentives from the public sector are required.

One of the main reasons for supporting lignocellulosic biorefineries was to achieve a high biomass utilization efficiency and to avoid unused bio-waste streams. Is this still a real argument?

If the lignocellulosic biorefinery mainly produces drop-in commodity chemicals, the biomass utilization efficiency can be low. We should not forget the highly efficient biomass utilization in the sugar and starch as well as in the pulp and paper industries. These existing plants also count as biorefineries optimised for high efficiency and they are running without any incentives. All parts of the biomass are utilized and no bio-waste is left over.

Smart, Small and Clever: New Bio-Based Building-Blocks and Innovative Pathways can Utilize the Full Potential of Functionalized Platform Molecules

Already today, the production of bio-based chemicals accounts for about €48 billion of turnover in the European Union (2013), as figure 1 (right) clearly demonstrates. And almost all of these chemicals are not drop-in chemicals, but bio-based dedicated speciality chemicals. With new and also known technologies such as biotechnology, chemical modification and extraction, and with new bio-based building-blocks with new functionalities, this amount can be considerably expanded.

Emerging strategies imply new building blocks and chemicals, new value chains, new investment in plants and infrastructure. These new building blocks are often produced by new processes, especially by industrial biotechnology using yeast/fungi, bacteria and enzymes to produce chemicals such as succinic or lactic acid in an efficient way. New emerging strategies based on biomass can take advantage of utilizing higher levels of structure already provided by nature. Industrial biotechnology is becoming an important biomass transformation technology: highly specific transformations can be accomplished under mild reaction conditions with often very high yields. Currently only 5-10% of all processes for biomass transformation in the chemical and material sectors are conducted according to biotechnological approaches, but the tendency is strongly increasing. (Mathijs et al. 2015)

Next to industrial biotechnology also the extraction of high value complex biomolecules is an important utilisation pathway, which can often be processed before or parallel to other pathways of utilisation. From several biomass sources, waste streams and residues extractable compounds are available and partly already in use. This is especially true for pine chemicals from wood residues and waste streams from the pulp and paper industry, mainly tall oil derived chemicals used for cleaning agents, solvents, lubricants, paints, adhesives and more. Another example are grape residues (pomace) containing Resveratrol, Polyphenols and Tannins, used in paints, tanning agents and nutraceuticals. There are many more examples and the extractable compounds are always of high value and can be used in several utilisation areas. (Mathijs et al. 2015).

Compared to drop-in commodity chemicals, bio-based dedicated pathways are more efficient, utilising not only the carbon in the biomass, but the whole biomass – carbon, oxygen, hydrogen and nitrogen. This is reflected in a high biomass utilization efficiency (BUE), see figure 4. Most of the new building blocks can be found on the top of the diagram and most of the drop-ins at the lower end (Iffland et al. 2015).

But there is also an interesting group of drop-in chemicals, partly fine chemicals, but also some smaller commodities with a high utilization efficiency. For those chemicals the traditional petrochemical pathways are complex and long, whereas new biotechnology pathways could be very short and efficient.

BUE calculations reflect a theoretical approach that has real life implications, for example for the land use efficiency of different bio-based chemicals (Iffland et al. 2015). “Bio-based product pathways with a higher BUE need smaller areas of cultivation for the same output compared to pathways with a lower BUE, which shows the BUE has a direct correlation with the land efficiency and the amount of land necessary to produce a certain product. For example, to produce the same amount of PE and PLA from sugar cane, one needs almost twice the cultivation area for PE than PLA” (Iffland et al. 2015).

The typical production capacity for bio-based dedicated chemicals is 20,000 to 40,000 t per year (such as the new BioAmber 30,000 t/y succinic acid plant in Canada), but also smaller plants (< 5,000 t/y) are on the market producing high-value specialities. The demand for biomass of those small and medium sized production plants can be met locally. This means that many locations close to the local biomass origin are suitable for production plants. “It is fundamental that biomass be locally sourced in order for the integrated biorefineries to be truly connected with the nearby environment” (Cayuela 2015).

Many SMEs are involved in bio-based dedicated processes, as Philp 2015 mentioned “... the small companies trying to make a bio-based chemical commercially often opt for high-value chemicals with low production volume.”

The hottest biomass dedicated and promising building-blocks, polymers and materials are listed below (based on Mathijs et al. 2015 and several other sources).

New bio-based chemicals among others:

- Glycerol and derivates, Hydropropionic acid and aldehyde, Itaconic acid, Farnesene, Furans (HMF, Furfural, FDCA), Lactid acid, Levulinic acid, Sorbitol, Succinic acid, Xylitol;

- PEF, PHA, PLA; PA (10,10, 10,12 and 12,12),

- Bio-based lubricants and surfactants (with already a yearly growth between 5 and 10%; eg. Sophoro- and Rhamnolipids, Alkylpolyglycosides);

- Cellulose fibres (with already a yearly growth between 5 and 10%), Nano- and microcellulose.

- Drop-in chemicals with new biotechnology pathways and high biomass utilization efficiency, for example:

- Acetic acid, Acrylic acid, Adipic acid, Butanediol, Butadiene, Isoprene;

- PA (6,6), PDO, PBS.

These bio-based chemicals and polymers fulfil the promises of the Bio-based Economy: increasing and maintaining the bio-based value, new functionalities (depending on the chemical/polymer: less unwanted by-products, less toxic for the environment, biodegradable), new and improved processes (biotechnology, extraction, new catalytic processes; better space/time yield, less reaction steps and/or energy required because reactions can be executed at temperatures around ca. 37 degrees without the need for a e.g. rare metal catalyst, no need to use toxic solvents), delivering solutions for Green and Sustainable Chemistry and Circular Economy; and also contributing to mitigating climate change by substitution of petrochemicals with higher GHG emissions. Bringing new business opportunities, investment and employment to rural areas, regional development and SMEs. And finally, optimizing the whole utilization of biomass through new and integrated biorefinery concepts.

From our point of view, a successful Bio-based Economy, which is accepted by the public and NGOs, should focus on the bio-based dedicated chemicals and materials described above, providing the consumer and the environment with proven advantages – including the reduction of GHG emissions.

The Sustainable Feedstock Question: Food or Non-Food Biomass for Bio-Based Products?

A recent strategy to sustain food security is the use of biomass waste streams and residues, which are not utilized so far, for the production of bio-based products. The problem is that most of the biomass waste streams are already utilized (an often overlooked fact) and the really not-utilized waste streams are more limited in volumes and properties than normally expected.

As producers rely on a steady supply of raw materials with sufficient quantity and quality characteristics to reasonable prices, the production of bio-based products is strongly connected to wood or agricultural biomass. But if it comes to agricultural crops, it is more a question of available land for their cultivation, than of being a food or non-food crop to use them. The use of non-food biomass is not related to improved food security – Carus et al. 2013 already made a comprehensive analysis of this topic. Imagine a huge biorefinery with a demand of biomass coming from approx. 50,000 ha. What is better for food security? To grow non-food crops, which often even need more land than food crops for the same amount of suitable molecules, or to grow additional food crops, which can be utilized for food if necessary in a food crisis?

The best feedstock solution seems to be to use local biomass in small and medium sized plants, to utilize biomass waste streams, additionally grown food crops (especially for highly efficient dedicated processes), second generation lignocellulosic biomass and also third generation algae for specific high-value applications. The best choice depends on the region and the targeted processes and products (Bruins and Sanders 2012).

“Today, first generation feedstocks such as industrial cane sugar, sugar beet, corn and cassava are used for producing lactic acid. They are grown following principles of sustainable agriculture and have a high yield per hectare of land used. These highly efficient feedstocks are – and will most likely remain – a good choice for lactic acid and PLA production. Corbion Purac is the first company in the world to have made PLA from second generation feedstocks, optimizing the lactic acid fermentation process to fit the special characteristics of the biomass. In the future, these alternative feedstocks can have a high impact on the biochemical and bioplastics industries.” (Corbion 2015)

Next to the described feedstocks, also the direct use of CO2 with bacteria, algae or chemical processes is becoming a real alternative – for some chemicals and polymers as well as especially for fuels. It will be important to analyse from an environmental and economic point of view, for which pathways CO2 is a better feedstock and for which pathways biomass will be the first choice also in the long-time future.

Future Outlook on Circular Economy

When Europe develops its Circular Economy, it needs to keep the bio-based economy in mind that has some specific challenges, but is also more integrated in our everyday, linear-economy life than many researchers and policy-makers think. As mentioned above, the cascading use of biomass is clearly a strong link between Bio-based and Circular Economy which is not supported by the existing political framework. Currently, incentives are only given for bioenergy and biofuels, hindering a more resource efficient use of biomass in cascades.

When the European Commission officially launched their Circular Economy package in December 2015, the utilization of biomass and cascading use was acknowledged in two sections:

“In a circular economy, a cascading use of renewable resources, with several reuse and recycling cycles, should be encouraged where appropriate. Biobased materials, such as for example wood, can be used in multiple ways, and reuse and recycling can take place several times. This goes together with the application of the waste hierarchy and, more generally, options that result in the best overall environmental outcome. National measures such as extended producer responsibility schemes for furniture or wood packaging, or separate collection of wood can have a positive impact. [...] The bio-based sector has also shown its potential for innovation in new materials, chemicals and processes, which can be an integral part of the circular economy. Realising this potential depends in particular on investment in integrated bio-refineries, capable of processing biomass and bio-waste for different end-uses. The EU is supporting such investments and other innovative bio economy-based projects through research funding” (European Commission 2015).

“The Commission will promote efficient use of bio-based resources through a series of measures including guidance and dissemination of best practices on the cascading use of biomass and support for innovation in the bioeconomy. The revised legislative proposals on waste contains a target for recycling wood packaging and a provision to ensure the separate collection of biowaste” (European Commission 2015).

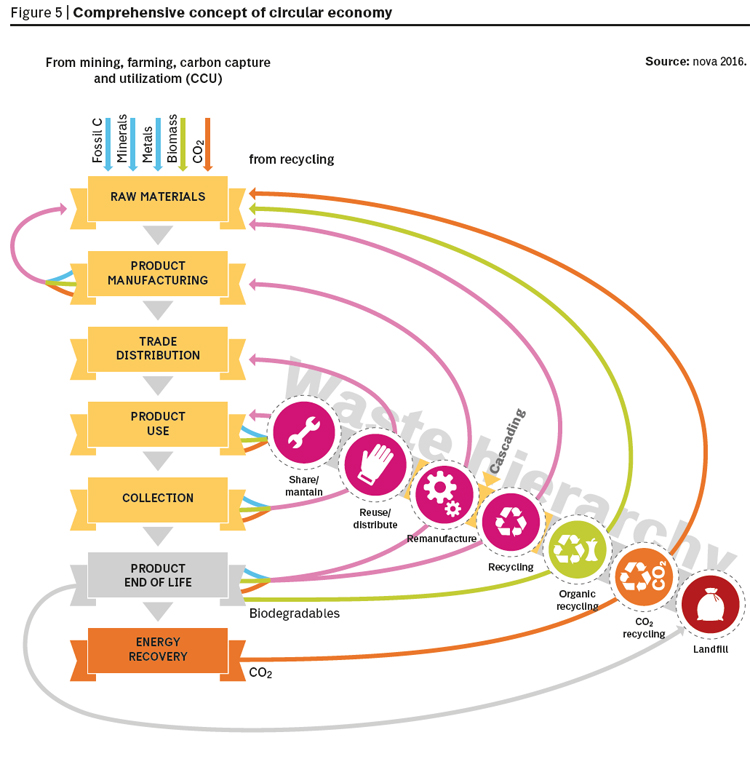

It would go beyond the scope of this article to make a detailed analysis of every aspect that needs to be addressed if Europe aims for a sound integration of the bio-based economy into the Circular Economy. However, the following graph (figure 5) is our contribution to the debate by offering an illustration that for the first time integrates the bio-based sector fully into the Circular Economy. Some of the currently popular graphs that describe the future Circular-Economy differentiate for example between cycles of biological materials and technical materials (Ellen MacArthur 2013), which is not an accurate depiction of actual resource flows. For that reason, our illustration includes all kinds of material streams and shows all different utilization routes belonging to a Circular Economy. Organic recycling (= biodegradation) and even the capture and utilization of CO2 from industrial processes or the atmosphere are included to provide a truly Comprehensive Concept of Circular Economy.

nova-Institute, www.nova-institut.de

Bibliography

- ACHEMA (2015), Summary of the event EU-Bioeconomy and HORIZON 2020 revisted: How far have we come since ACHEMA 2012?, Frankfurt, 2015-06-18

- BiofuelDigest (2016), The 30 Hottest Molecules survey, January 2016 (www.biofuelsdigest.com)

- BIO-TIC (2015), A roadmap to thriving industrial biotechnology sector in Europe. FP7 project (www.industrialbiotech-europe.eu)

- Bruins, M. E., & Sanders, J. P. (2012), “Small-scale processing of biomass for biorefinery. Biofuels”, Bioproducts and Biorefining, 6(2), 135-145

- Carus, M., Carrez, D., Kaeb, H., Ravenstijn, J., Venus, J. (2011), Level Playing Field for Bio-based Chemistry and Materials. nova paper #1 on bio-based economy, Hürth 2011-07. Download at www.bio-based.eu/nova-papers

- Carus, M. and Dammer, L. (2013), Food or non-food: Which agricultural feedstocks are best for industrial uses? nova paper #2 on bio-based economy, Hürth 2013-07. Download at www.bio-based.eu/nova-papers

- Carus, M., Eder, A., Beckmann, J. (2014), GreenPremium prices along the value chain of bio-based products. Hürth 2014. nova paper #3 on bio-based economy, Hürth 2014-05. Download at www.bio-based.eu/nova-papers

- Carus, M., Dammer, L., Essel, R. (2015), Options for Designing the Political Framework of the European Bio-based Economy. nova paper #6 on bio-based economy, Hürth 2015-06. Download at www.bio-based.eu/nova-papers

- Cayuela, R. (2015), “The New Chemistry Is Worth $80 Trillion, interview with Rafael Cayuela”, In Renewables Matter – International magazine of the bioeconomy and the circular economy, 4, June 2015

- Corbion (2015), Corbion Purac successfully develops PLA resin from second generation feedstocks, press release 2015-10-13

- Ellen MacArthur Foundation (2013), Towards the Circular Economy. Opportunities for the consumer goods sector. Isle of Wight 2013

- European Commission (2012), Innovating for Sustainable Growth – A Bioeconomy for Europe, European Commission, DG for Research and Innovation, Brussels 2012

- European Commission (2015), Closing the loop – An EU action plan for the circular economy, European Commission, Brussels, December 2015

- GBS (2015), Communiqué Global Bioeconomy Summit 2015 – Making Bioeconomy Work for Sustainable Development. Berlin, November 2015

- Iffland, K., Sherwood, J., Carus M., Raschka, A., Farmer, T., Clark, J. (2015), Definition, Calculation and Comparison of the “Biomass Utilization Efficiency (BUE)” of Various Bio-based Chemicals, Polymers and Fuels. nova paper #8 on bio-based economy, Hürth 2015-11. Download at www.bio-based.eu/nova-papers

- Mathijs, E. (2015), Sustainable Agriculture, Forestry and Fisheries in the Bioeconomy – A Challenge for Europe. 4th SCAR Foresight Exercise, Brussels, October 2015

- NISCluster (2015), The bioeconomy must move away from drop-in thinking! Newsletter of the NISCluster, Finland, November 2015

- Philp, J. (2015), Balancing the bioeconomy: supporting biofuels and bio-based materials in public policy. The Royal Society of Chemistry. August 2015

- Pietikäinen, S. (2015), “Championing the Circular Cause, interview with Sirpa Pietikäinen” edited by Joanna Dupont-Inglis, In Renewables Matter – International magazine of the bioeconomy and the circular economy, 4, June 2015

- VCI (2015), Basischemie 2030 – Aktualisierte Analyse zur Zukunft der Basischemie, VCI, Frankfurt, October 2015

- Yoon, A. (2015), Increasing Demand for Wood-Based Biofuel Threatens U.S. Forests, TriplePundit (www.triplepundit.com/2015/11/increasing-demand-wood-based-biofuel-threatens-u-s-forests/)